Top 5 Questions to Ask your Mortgage Lender

KellyHudsonMortgages • December 19, 2016

The decision to purchase your first home can be a huge, life-changing event and you need to know exactly what you are getting into. Being prepared is the first step

When you are ready to buy a home, and you need mortgage there i s a lot of information to research and understand. I’ve put together a list of questions to help you make an educated decision regarding choosing the right mortgage lender for your situation

- How the penalties are calculated if I break my mortgage early? Specifically ask what rate the lender uses to calculate the “interest rate differential”.

- Typically, banks & credit unions have “posted rates” which are higher than their actual mortgage rates. They use these higher “posted rates” to calculate your penalty if you need to break your mortgage early.

- The inflated posted rate penalty can be 3- 5 times higher than a mortgage lender that does NOT inflate their posted rate.

- 60% of people break their mortgage before their term is over, so asking this question could save you thousands of dollars.

- Mortgage Penalties – Ouch… How Much??

- Is this a “collateral charge or revolving” mortgage or a conventional mortgage?

Many lenders have started putting all

of their mortgages into what is called a “collateral charge”. For the right client with a lot of equity in their home, this product can be very useful. Most big banks and credit unions only offer collateral charge mortgages.

- The disadvantage of a collateral charge mortgage is that you cannot “switch” it to another lender once your term is over at NO CHARGE.

- You have to pay discharge a collateral charge mortgage and re-register a new mortgage with your new lender, which will cost you an around $1000 for legal fees and appraisal costs. It will cost you to leave your current lender… which makes these mortgages sticky and hard to get out of.

- Collateral vs Conventional Mortgages… What the Banks don’t want you to know…

- Can I “blend and extend” my mortgage if I buy another home?

- Most variable rate mortgages cannot be “blended”. Typically, the penalty to break a variable is 3 months’ interest. Some lenders have quietly changed their policies and now instead of allowing you to add new money to a mortgage in the event of a new purchase, they require you to break your mortgage and pay the full penalty.

- Some clients have been caught off guard by sneaky lenders who don’t tell them this until only a few days before close, at which time it’s too late to switch lenders.

- What happens to my mortgage life and/or disability insurance if I switch to a new lender at the end of my term?

- For people who take out Mortgage insurance offered by their bank or lender, the challenge is that if you want to “switch” your mortgage to another lender at the end of your term, you have to re-apply for insurance.

- The downside to this is that you’ll be five years older (more expensive), and if you have developed any health issues during the previous 5 years, you may not be able to requalify for Mortgage insurance.

- Purchasing mortgage insurance, separate from your lender, stays in place the whole time you have your mortgage, it doesn’t matter who your lender is.

- What happens at the completion of your mortgage term (typically 5 years)?

- Most banks know that clients won’t negotiate the best rates so typically their renewal offer isn’t competitive.

- Working with an independent mortgage expert keeps lenders honest about rates. An independent mortgage expert will make sure you have the best options available every time your mortgage comes due.

Would you like more information regarding mortgages? Give me a call and let’s have a chat.

Kelly Hudson

Mortgage Expert

Mobile: 604-312-5009

Kelly@KellyHudsonMortgages.com

www.KellyHudsonMortgages.com

Kelly Hudson

MORTGAGE ARCHITECTS

RECENT POSTS

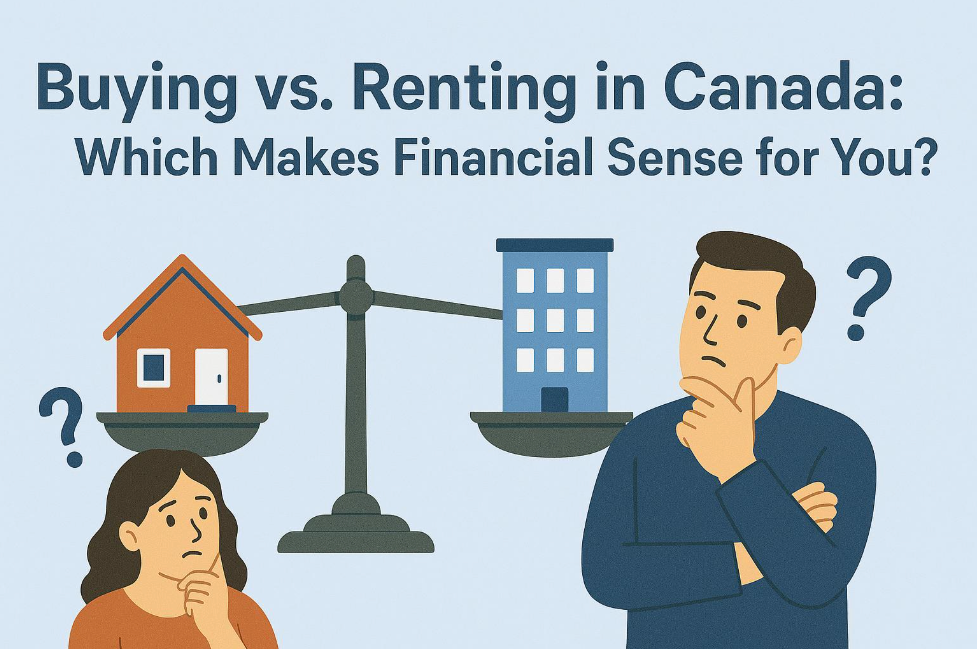

Are you debating whether it's smarter to rent or buy a home in Canada? It's a common question, and the answer depends on your personal situation. Both renting and buying have their pros and cons, but for most people, homeownership tends to offer substantial long-term benefits. Let’s explore both options clearly, so you can confidently decide what’s best for you. Advantages of Buying a Home 1. Personal Freedom and Customization Owning your home means having the freedom to personalize your living space. Dreaming of a bold paint colour or unique flooring? Go ahead—your home, your rules! 2. Building Equity and Wealth Each mortgage payment you make is an investment in yourself. Over time, your home typically appreciates in value, increasing your equity. This can become a significant asset that helps secure your financial future. 3. Stability and Security Owning offers peace of mind. You don’t need to worry about sudden rent hikes or eviction notices. Your home remains yours until you decide otherwise. 4. Long-Term Financial Benefits Homeownership acts as forced savings. Unlike renting, every mortgage payment moves you closer to outright ownership, building a financial foundation that can support you and your family for years to come. Challenges of Buying a Home 1. Upfront Costs Buying comes with significant initial costs, including a down payment, legal fees, home inspection, appraisal, moving expenses, etc. 2. Responsibility for Maintenance Owning a home means you're responsible for maintenance and repairs. This can sometimes be costly and inconvenient. 3. Reduced Flexibility Selling a home typically takes time, which can limit your flexibility if you need or want to relocate quickly. Advantages of Renting 1. Easy Mobility Renting offers flexibility to relocate easily, beneficial for frequent job changes or lifestyle adjustments. 2. Fewer Responsibilities Repairs and maintenance are generally your landlord’s responsibility, reducing stress and unexpected expenses. 3. Lower Initial Costs Renting typically requires just a security deposit and the first month's rent, making it easier financially at the start. Downsides of Renting 1. No Equity Building Rent payments do not contribute to your equity. Instead, you’re effectively paying your landlord’s mortgage, offering no long-term financial return. 2. Restrictions and Rules Landlords often impose limitations, such as no pets or restrictions on decorating, making it challenging to feel fully at home. 3. Instability and Uncertainty Renters may face sudden rent increases or eviction if the landlord decides to sell or repurpose the property, disrupting your life significantly.

Since March 2022, mortgage rates in Canada have risen significantly, raising concerns for homeowners and potential buyers. But what drives these changes, and how do they impact your choice between fixed and variable mortgage rates? Let's simplify this important financial topic.