Mortgage Articles

If you’re buying a condo, townhouse, or bare-land strata property in BC, there’s one document many buyers overlook: the depreciation report. Strata depreciation report requirements - Province of British Columbia And honestly… it’s one of the most important documents you can review before buying. I see this all the time with clients. Some buyers carefully review it. Others quickly skim through it just to “check the box.” But this report can affect: your mortgage approval future repair costs special levies insurance and how stressful ownership may become later So, let’s break it down in simple, real-world language.

Decisions relating to real estate can have significant financial and legal consequences. Before deciding how to share ownership of what is likely one of the largest investments of your life, I recommend consulting a real estate lawyer. Many Canadians purchase property together — including spouses, common-law partners, family members, friends, and business partners. Because ownership structure affects estate planning, taxes, creditor exposure, and control over the property, it’s important to understand your options before you sign. In Canadian property law, there are two primary forms of co-ownership: Joint Tenancy Tenancy in Common While these terms may sound similar, they have very different legal and financial effects — particularly if one owner dies, sells their interest, separates, or faces creditor claims.

If you’re 55 or older and own your home, chances are you’ve heard about reverse mortgages. Sometimes they’re described as a “retirement lifesaver.” Other times they sound risky or confusing. The truth? They’re neither magical nor terrible. They’re simply a financial tool — and like any tool, they work well in some situations and not so well in others – EDUCATION is the key! Let’s break it down in plain English. So… What Is a Reverse Mortgage? A reverse mortgage allows you to borrow money against the value of your home — without making monthly mortgage payments. Instead of you paying the lender every month, the interest gets added to the balance. The loan is typically repaid when: The home is sold You move out permanently Or you pass away In Canada, reverse mortgages are currently offered by: HomeEquity Bank (CHIP Reverse Mortgage) Equitable Bank Bloom Financial You still own your home and your name stays on title. That part often surprises people. How It Works (Simple Version) To qualify: You must be 55 or older You must own your home (you can still have a regular mortgage — it just needs to be paid out) You can usually borrow up to about 55% of your home’s value (the older you are, the more you may qualify for) You don’t make monthly payments. But you must continue to: Pay property taxes Keep home insurance in place Maintain the home The money you receive is tax-free. It can come as: A lump sum Monthly advances Or a combination of both That flexibility is one reason many retirees like this option. Why Do People Consider Reverse Mortgages? Most of the homeowners I speak with aren’t looking for luxury spending money. They’re trying to solve real life situations: Covering rising living costs Paying off debt before retirement Managing health or care expenses Staying in their home longer Helping adult children with a down payment For many Canadians, their house is their largest asset — but it doesn’t create monthly income. A reverse mortgage turns some of that home equity into usable cash. The Pros (The Reasons People Like Them) 1. No Monthly Mortgage Payments This is the big one. If you’re living on CPP and OAS, removing a monthly mortgage payment can dramatically reduce stress. Cash flow improves immediately. 2. You Can Stay in Your Home Most people I meet don’t want to move. They love their neighborhood. Their friends are nearby. Family visits often. A reverse mortgage can allow you to age in place instead of selling before you’re ready. 3. The Money Is Tax-Free Because it’s borrowed money — not income — it does not affect: Old Age Security (OAS) Guaranteed Income Supplement (GIS) That’s a major advantage compared to withdrawing from investments. There are no rules about spending. Some clients use the funds to stay in place – health care at home. Some clients renovate. Some travel. Some gift funds to children. Some simply create a safety cushion. It’s your equity – you decide. 5. You Keep Ownership The bank does not own your home. As long as you live in your home, maintain it, insure it, and pay property taxes — you own your home and can stay. 6. No Negative Equity Guarantee In Canada, reverse mortgages include protection so that you (or your estate) will never owe more than the home is worth — even if property values decline. That protection matters.

What Is BC Assessment? Every January, British Columbia homeowners receive their annual Property Assessment Notice . BC Assessment is a provincial Crown corporation responsible for valuing all real estate in British Columbia for property tax purposes. Each year, BC Assessment provides an estimate of a property’s fair market value as of July 1 of the previous year . 👉 To view the most recent assessment for any property, visit the BC Assessment website and search by address. Important things to understand about BC Assessments Timing matters. Your 2026 assessment reflects an estimated market value as of July 1, 2025, not today. Markets change quickly. In active or volatile markets (like Greater Vancouver and the Fraser Valley), values can shift significantly in a matter of months. Mass appraisal methods are used. BC Assessment relies on algorithms and broad market data rather than a detailed, in-person inspection of your specific home. Because of this, an assessed value can differ — sometimes substantially — from: a lender-ordered mortgage appraisal, or a private real estate appraisal completed for buying or selling. BC real estate context (2026) As we move through 2026, BC housing markets continue to be influenced by: interest-rate expectations and changes by the Bank of Canada, affordability pressures, regional supply constraints, and local economic conditions. This means BC Assessment values should be used only as a starting point , not as a precise indicator of what a property will sell for or what a lender will accept as value. Bottom line: Do not rely on BC Assessment for the exact value of a property you’re planning to sell, purchase or refinance.

Foreign Home-Buyer Tax in BC: What You Need to Know as of Dec. 2025 (For informational purposes only – always confirm details with your accountant & lawyer before buying.)

Buying a home is one of the most important financial decisions you will make and tends to be stressful with all the new terminology. To help you understand the process and have confidence in your choices, check out the following common terms you will encounter during the home buying process. Amortization – Length of time…

Buying a home is one of the biggest financial moves you’ll ever make — and along with it comes a whole lot of new terms, rules, and (you guessed it) insurance . You might think “Mortgage insurance… how complicated can that be?” But once you start hearing about default insurance , mortgage life insurance , and home insurance , it’s easy to get lost in the fine print. Don’t worry — this guide breaks it all d own so you can feel confident about what each type does, what it costs, and why it matters.

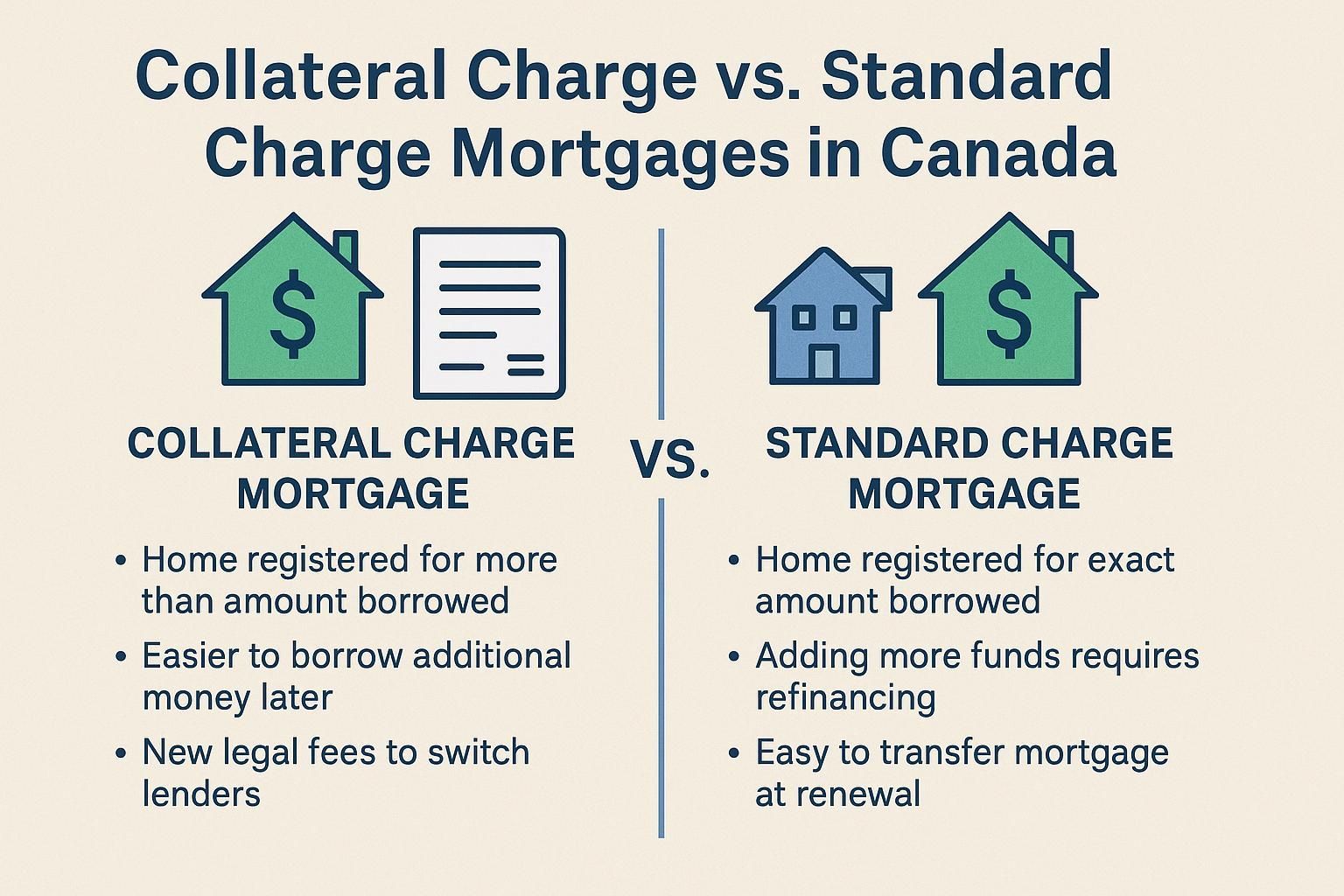

When you’re buying a home in Canada, you’ll hear a lot of new terms. One of those is how your mortgage is registered: as a standard charge or a collateral charge . This choice matters because it affects your flexibility, your costs if you ever switch lenders, and how easy it is to borrow more money later. Let’s break it down in simple terms.

Greater Vancouver Property Management Fees – What You Need to Know